Fast, Free and No Risk

Fast, Free and No Risk

How Does a California Contractor License Bond Work? (Mechanics & Risk Explanation)

![]() Updated for 2026 Licensing Requirements

Updated for 2026 Licensing Requirements

Quick Answer: A California contractor license bond is a $25,000 financial guarantee required by the CSLB under Business & Professions Code §7071.6. It is a three-party agreement where the Surety (Bond Company) acts as a line of credit, guaranteeing the Contractor’s legal compliance. If a valid claim is filed (e.g., by a homeowner or employee), the surety may pay the damages up to $25,000, and the contractor is legally required to reimburse the surety for the full claim amount and related costs.

In simple terms, a contractor license bond works as a financial guarantee that you will follow California construction laws—or pay the consequences if you don’t. Unlike insurance, a contractor license bond does not protect your business—it guarantees your compliance and requires repayment if a claim is paid.

California Contractor Bond Requirements, Cost, and CSLB Filing Guide (2026)

How a California Contractor License Bond Works – Key Facts

- Required Bond Amount: $25,000

- Required By: California Contractors State License Board (CSLB)

- Legal Authority: California Business & Professions Code § 7071.6

- Type of Agreement: Three-party agreement between the contractor, the CSLB, and the surety company

- Who the Bond Protects: Consumers, employees, subcontractors, and the public — not the contractor

- How It Works: The surety may pay valid claims up to $25,000, then seeks full reimbursement from the contractor

- Financial Reality: A contractor license bond is not insurance; the contractor remains financially responsible for claims

- Claim Process: CSLB Bond Claim: How to Handle, Defend & Reinstate Your License

- Repayment Obligation: Contractors must repay the surety for claim payouts and related costs under the indemnity agreement

- License Risk: Failure to repay the surety can result in license suspension

- Key Takeaway: A contractor bond is a compliance guarantee, not financial protection for the contractor’s business

Quick Summary:

– You buy the bond to stay compliant

– The surety guarantees your obligations

– If a claim is paid, you must repay it in full

▶ View Transcript

[00:00] How does a California contractor license bond actually work?

[00:02] It’s not insurance—and misunderstanding that can cost you thousands.

[00:06] A contractor license bond is a $25,000 financial guarantee required by the CSLB.

[00:10] It’s a three-party agreement between you, the state, and a surety company.

[00:14] Here’s how it works step by step.

[00:16] First, you purchase the bond and the surety files it with the CSLB so your license can become active.

[00:21] Then, if something goes wrong—like unpaid wages or a contract violation—a claim can be filed against your bond.

[00:27] The surety investigates the claim to determine if it’s valid.

[00:30] If it is, the surety may pay the claim—up to $25,000.

[00:34] But here’s the part most contractors don’t realize.

[00:37] You are legally required to repay the surety for every dollar they pay out.

[00:41] That includes fees and costs—not just the claim itself.

[00:44] If you don’t repay, your license can be suspended.

[00:47] So what’s the takeaway?

[00:49] A contractor bond protects the public—not your business.

[00:52] It guarantees your compliance—and makes you financially responsible if you violate the law.

[00:56] Understanding this is critical to managing your risk as a contractor. Get a quote today at SuretyFirst.com

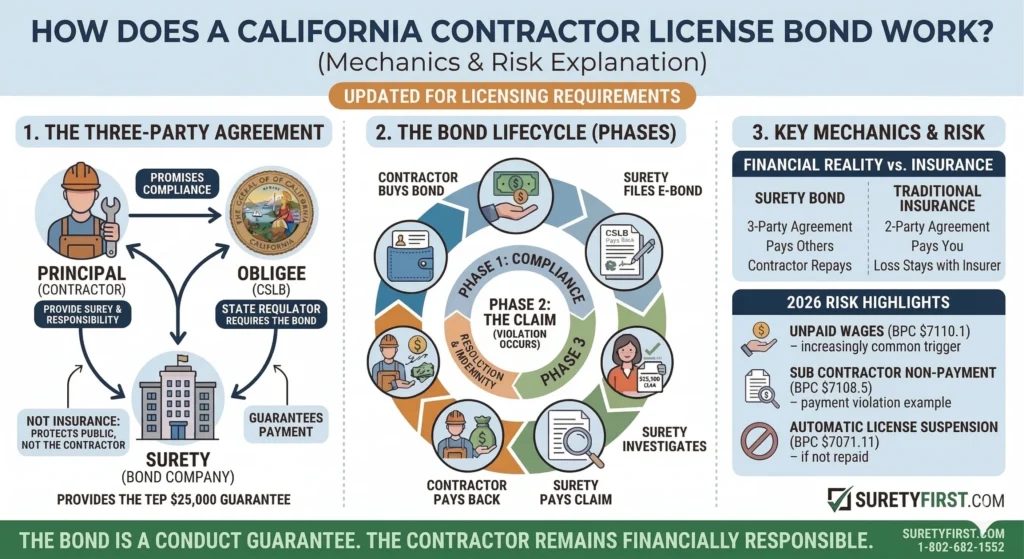

The Three Legal Parties (The Tri-Party Agreement)

Unlike a simple two-party insurance contract, a surety bond is a complex three-party legal structure. Understanding who holds the financial risk is the key to knowing how the bond works.

-

1. The Principal (You): The licensed contractor who purchases the bond and promises to obey all California contracting laws (BPC §7000+).

-

2. The Obligee (CSLB): The California Contractors State License Board. As the government regulator, they require the bond to protect the public, not the contractor.

-

3. The Surety (Bond Company): The financial institution that provides the $25,000 guarantee and will pay a valid claim initially.

Have questions about what a contractor bond is? See our guide:

What Is a California Contractor License Bond?

How a California Contractor Bond Works (Step-by-Step)

Here is the exact lifecycle of a California contractor license bond, from purchase to claim resolution.

Phase 1: Compliance

-

Contractor Purchases Bond: The contractor applies for the bond and pays a small annual premium.

-

Surety Files E-Bond with CSLB: The surety company electronically files CSLB Form 13B-1 directly with the Board (physical/paper bonds are no longer accepted).

-

License Becomes Active: Once the CSLB processes the filing, your license status is updated to “Active.”

To learn more about how much California contractor license bonds cost, see our guide:

How Much Does a California Contractor License Bond Cost?

Phase 2: The Claim (If a Violation Occurs)

-

Claim is Filed: A Homeowner, Employee (for unpaid wages/benefits, a 2026 CSLB priority), or Subcontractor files a financial claim against the $25,000 bond (under BPC §7071.5).

-

Surety Investigates: The surety company does not automatically pay. They conduct a thorough investigation to verify if a violation of the construction contract or license law actually occurred.

To learn more about contractor license bond claims, see our guide:

CSLB Bond Claim: How to Handle, Defend & Reinstate Your License

Phase 3: Resolution & Indemnity

-

Surety Pays Claim: If the surety determines the claim is valid, they will pay the claimant up to the $25,000 bond limit.

-

Contractor Must Repay (Indemnity): The most critical and widely misunderstood component of how a California contractor license bond works is the Indemnity Agreement. This is the legal contract you sign with the surety company when you purchase the bond.

Indemnity means that the Contractor (Principal) agrees to completely financially hold harmless the Surety (Bond Company) for any claims paid out on their behalf.

The Core Distinction: Financial Liability

-

-

Traditional Insurance (e.g., General Liability): When an insurance company pays a claim (e.g., for property damage), they generally “take the loss.” The contractor is not required to pay them back.

-

A Surety Bond: When a surety pays a claim, they do not take the loss. Under your Indemnity Agreement, you are legally required to reimburse the surety for every dollar they spend on your behalf.

-

License Suspension: If you do not pay the surety back, your license will be automatically suspended under BPC §7071.11 until a new bond is filed and the surety is made whole.

Learn more about contractor license bond suspensions here:

CSLB Bond Lapses: How to Fix an Automatic License Suspension

The Fundamental Difference: Why It’s Not Insurance

Unlike insurance, a contractor license bond does not protect the contractor—it protects the public, and the contractor must repay any claims. See our guide explaining what contractors’ liability insurance is here:

Contractor General Liability Insurance: Cost, Coverage & Requirements (2026 Guide)

Real-World Example (2026 Focus: Unpaid Wages)

To understand the mechanics, consider a scenario that is increasingly common in 2026 due to stricter wage theft enforcement (BPC §7110.1).

-

The Scenario: A general contractor fails to pay a skilled worker $10,000 in fringe benefits as required by their employment agreement.

-

The Claim: The employee files a claim against the contractor’s $25,000 license bond for the unpaid $10,000.

-

How it Works: The Surety investigates, confirms the non-payment violation, and pays the employee $10,000 directly.

-

The Contractor’s Debt: The contractor now owes the surety company $10,000 plus legal/administrative fees. Their license will be suspended by the CSLB until the debt is cleared.

Key Takeaway

The contractor license bond is a conduct guarantee, not protection for your business. It is the state’s tool to ensure that if you violate the law, there is a dedicated fund available to compensate harmed parties—at your expense.

Frequently Asked Questions

How does a California contractor license bond actually work?

A contractor license bond is a three-party agreement between the contractor (principal), the CSLB (obligee), and the surety company. The surety guarantees the contractor’s compliance with state laws and pays valid claims if violations occur—then seeks full reimbursement from the contractor.

What triggers a claim against a contractor license bond?

A claim is triggered when a contractor violates licensing laws or contractual obligations, such as failing to complete work properly, not paying subcontractors, or failing to pay employee wages.

What happens when a claim is filed?

The surety investigates the claim to determine validity. If the claim is valid, the surety pays the claimant up to the bond limit, typically $25,000 for a California contractor license bond.

Do contractors have to repay bond claims?

Yes. Contractors must repay the surety for any claim paid, including legal and administrative costs. The bond acts as a financial guarantee—not insurance for the contractor.

Who does a contractor license bond protect?

The bond protects consumers, employees, subcontractors, and the state—not the contractor. It ensures there is a financial mechanism to compensate harmed parties.

What happens if a contractor does not repay a bond claim?

If the contractor fails to repay the surety, their license can be suspended and they may be unable to obtain a new bond until the debt is resolved.

Is a contractor license bond the same as insurance?

No. A contractor license bond guarantees legal compliance, while insurance protects the contractor from certain risks. With a bond, the contractor remains financially responsible for claims.

Related California Contractor Bond Guides

-

- California Contractor Bond Requirements, Cost, and CSLB Filing Guide (2026)

- How to Get a CSLB License Bond with Bad Credit

- CSLB Form 13B-1 Explained

- Who Needs a Contractor License Bond in California?

- Bond of Qualifying Individual (BQI): Requirements, Cost, and CSLB Filing Guide (2026)

- California LLC Employee/Worker Bond – Cost, Requirements & CSLB Filing Guide (2026)

Reviewed by: Jeremy Schaedler

Principal – Surety First Insurance Services

As principal at Surety First, Jeremy Schaedler has specialized in contractor license bonds and construction insurance since 2006. CA License: 0f06277

This information is for general informational purposes only and does not constitute legal advice. Licensing and insurance requirements may change. Contractors should verify current requirements directly with their state regulatory agency or consult qualified legal counsel.

Management team at Surety First Insurance Services, specializing in contractor license bonds and commercial insurance for contractors.

Why Contractors Choose Surety First

- Specializing in contractor bonds and insurance since 2006 (20,000+ served)

- A-rated surety markets

- Fast approvals, often within minutes

- Electronic CSLB filing

- Serving contractors across CA, OR, WA, NV, AZ

Phone: 1-800-682-1552

Website: suretyfirst.com

Sources

California Business & Professions Code § 7071.6 (Contractor License Bond Requirement)

California Business & Professions Code § 7071.5 (Bond Claims)

California Business & Professions Code § 7071.11 (License Suspension)

California Contractors State License Board (CSLB) – Bond Information