Fast, Free and No Risk

Fast, Free and No Risk

Arizona Contractor Bond Credit Score Requirements

![]()

Updated for 2026 Requirements

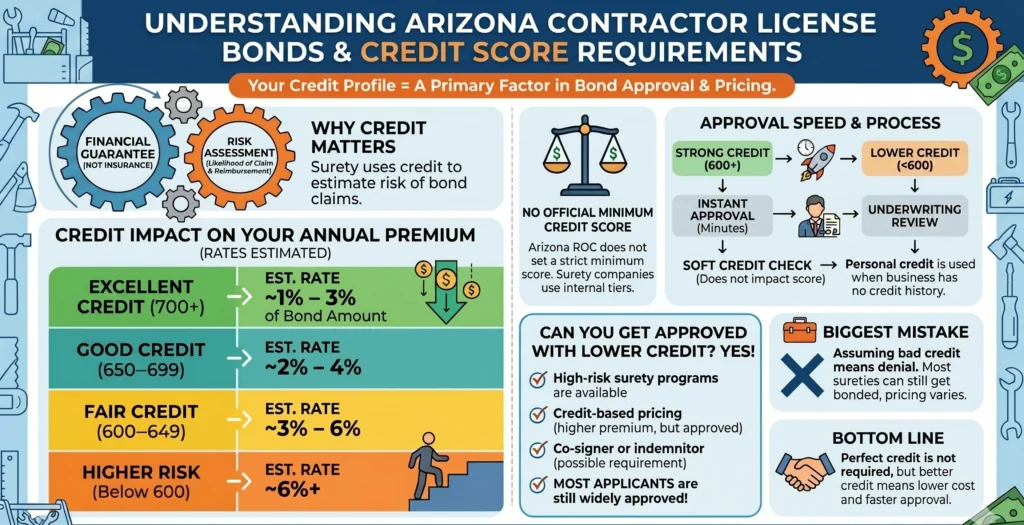

Quick Answer: Your credit profile is one of the primary factors used to approve and price an Arizona contractor license bond. Surety companies use credit to estimate risk—specifically, the likelihood of a claim and whether the contractor will reimburse the surety if a claim is paid.

Unlike insurance, a contractor bond is a financial guarantee, not risk transfer. That’s why credit matters. The stronger your credit, the lower your rate and the easier your approval. The weaker your credit, the higher your premium—or the more underwriting review required.

The good news: most contractors—especially new applicants—can still get approved, even with less-than-perfect credit. Before diving into credit requirements and pricing, it’s important to understand the fundamentals of how Arizona contractor license bonds work and why they’re required. Arizona Contractor License Bond

Arizona Contractor Bond Credit Score Requirements – Key Facts

- Core Factor: Credit profile is one of the main factors used to approve and price an Arizona contractor license bond

- No Official Minimum: The Arizona ROC does not set a strict minimum credit score requirement.

- Best Rates: Contractors with stronger credit typically receive lower premiums and faster approval

- Lower Credit: Applicants with weaker credit can often still qualify, but may pay higher rates

- Common Approval Range: Most applicants with scores around 600+ are widely approved

- Below 600: Approval may still be possible through high-risk surety programs or underwriting review

- Soft Credit Pull: Most applications use a soft credit check that does not impact your score

- Approval Speed: Strong credit often leads to instant approval, while lower credit may require additional underwriting

- Pricing Impact: Better credit usually means lower annual premium; lower credit usually means higher cost

- Bond vs. Insurance: A contractor bond is a financial guarantee, not risk-transfer insurance

- New Contractors: Approval is usually based on personal credit, especially when business credit history is limited

- Biggest Mistake: Assuming bad credit means denial—most contractors can still get bonded, but pricing may vary

▶ View Transcript

[00:00] If you’re applying for an Arizona contractor license, your credit score plays a major role in your bond approval and cost.

[00:05] But here’s the truth—there’s no minimum credit score required to get bonded. Most contractors can still get approved, even with less-than-perfect credit.

[00:12] So what does your credit actually affect? Two things: your price and your approval speed.

[00:16] Strong credit—typically 700 and above—gets you the lowest rates and instant approval.

[00:21] Mid-range credit still qualifies quickly, just at slightly higher rates.

[00:25] And even if your score is below 600, you can often still get approved—you’ll just pay more and may go through underwriting.

[00:31] Contractor bonds are priced as a percentage of the bond amount. Better credit usually means 1 to 3 percent. Lower credit can be 6 percent or more.

[00:39] For example, a $10,000 bond could cost $100 a year with good credit—or $600 or more with lower credit.

[00:45] The key point: this isn’t insurance. A bond is a financial guarantee, so the surety uses your credit to measure risk.

[00:51] Bottom line—you don’t need perfect credit to get licensed. You just need to understand how your credit affects cost and approval.

[00:56] Visit SuretyFirst.com and start your Arizona contractor bond quote today.

What is the Minimum Credit Score for an AZ Contractor Bond?

There is no strict minimum credit score required by the Arizona ROC to obtain a contractor license bond. However, surety companies use internal credit tiers to determine eligibility and pricing.

Typical approval ranges:

- 700+ (Excellent Credit): Best rates, instant approval

- 650–699 (Good Credit): Standard rates, fast approval

- 600–649 (Fair Credit): Higher premiums, still widely approved

- Below 600 (Higher Risk): May require underwriting, higher cost

Most applicants are approved in the 600+ range, and even lower scores can often qualify through specialty or high-risk markets.

How Credit Scores Impact Your Premium and Approval Odds

Your credit score directly affects two things:

1. Your Bond Premium

Contractor bonds are typically priced as a percentage of the bond amount:

- Strong credit: ~1% – 3% of bond amount

- Average credit: ~3% – 6%

- Lower credit: ~6%+

Example:

- $10,000 bond

- Good credit: $100 – $300/year

- Lower credit: $600+/year

Understanding how your credit impacts pricing is key—but your actual bond amount is what ultimately determines your total cost. Arizona Contractor Bond Amount Requirements (ROC Guide)

2. Your Approval Speed

- Good credit → instant approval (minutes)

- Lower credit → underwriting review

In short: better credit = lower cost + faster approval

| Credit Tier | Credit Score Range | Approval Speed | Estimated Rate | Key Outcome |

|---|---|---|---|---|

| Excellent Credit | 700+ | Instant (minutes) | ~1% – 3% | Lowest cost, fastest approval – often instant online |

| Good Credit | 650 – 699 | Fast (same-day) | ~2% – 4% | Standard rates, quick approval – often instant online |

| Fair Credit | 600 – 649 | Fast to Moderate | ~3% – 6% | Higher cost, widely approved – often instant online |

| Higher Risk Credit | Below 600 | Underwriting review ~30 minutes | ~6%+ | Higher premiums, may require underwriter review |

Getting Approved for an AZ Bond with “Bad Credit” or No Credit

Even if your credit isn’t strong, approval is still possible.

Options include:

- High-risk surety programs

- Credit-based pricing tiers (higher premium, but still approved)

- Co-signer or indemnitor (in some cases)

Important points:

- Most contractor license bonds are still issued with minimal documentation

- You do not need perfect credit to get licensed

- The trade-off is usually cost, not eligibility

For new contractors with limited history, approval is often based on personal credit, not business credit.

Why Surety Companies Use Soft Credit Pulls for AZ Bonds

Most Arizona contractor license bond applications use a soft credit check, not a hard inquiry.

That means:

- ✔ No impact on your credit score

- ✔ No visible inquiry to lenders

- ✔ Fast approval decisions

Sureties use soft pulls because:

- Bond amounts are relatively small

- Risk is evaluated quickly through credit profile + application data

- The goal is speed and accessibility for licensing

Bottom Line

You don’t need perfect credit to get an Arizona contractor license bond—but your credit score will directly impact your cost and approval speed. Most contractors are approved quickly with a soft credit check, and even lower-credit applicants can secure a bond through specialized markets. The key is understanding how your credit affects pricing so you can get approved and keep your licensing process moving forward.

Once you understand how credit impacts your approval and cost, the next step is knowing exactly how to apply and get your bond issued quickly. How to Get an Arizona Contractor License Bond as a New Applicant

Ready to see your exact rate and get approved fast? Start your Arizona contractor bond quote in minutes.

Get a Arizona Bond Quote Now →

Frequently Asked Questions:

What credit score do I need for an Arizona contractor bond?

There is no official minimum set by the Arizona Registrar of Contractors. Most contractors are approved with scores above 600, but even lower scores can qualify through high-risk markets. Each surety uses their own rating system and credit score thresholds in determining rates.

Can I get approved with bad credit?

Yes. Approval is still possible with lower credit. You may pay a higher premium or go through underwriting, but most applicants can still obtain a bond.

How does my credit score affect my bond cost?

Your credit determines your rate:

- Strong credit: Lower rates

- Average credit: Average rates

- Lower credit: Higher rates

Better credit = lower cost.

Your credit score directly drives what you’ll pay—but understanding the full cost structure gives you the complete picture of your bond expense. How Much Does an Arizona Contractor License Bond Cost?

Does my credit affect approval speed?

Yes. Strong credit usually results in instant approval within minutes. Lower credit may require underwriting which typically takes 30 minutes or less.

Is there a difference between personal and business credit?

For most new contractors, approval is based on personal credit, not business credit. Established businesses may eventually use business financials, but personal credit is the primary factor early on.

Will applying for a bond hurt my credit score?

No. Most surety companies use a soft credit pull, which does not impact your credit score or show up as a hard inquiry.

Why do surety companies check credit for bonds?

Because a bond is a financial guarantee—not insurance. The surety evaluates your likelihood of repaying a claim if one occurs, and credit is the fastest way to assess that risk.

Credit is used to measure risk—but understanding how that risk turns into real bond claims is what ultimately protects your business. Arizona Contractor Bond Claims Explained: How Claims Work and How to Avoid Costly Mistakes

What happens if my credit is below 600?

You may still qualify, but expect higher premiums and possible underwriting review. Some cases may require additional documentation or a co-signer.

Can I improve my bond rate over time?

Yes. As your credit improves, you can often qualify for lower rates at renewal, reducing your annual bond cost.

What’s the biggest mistake contractors make with credit and bonds?

Assuming they won’t qualify due to low credit and not applying. In reality, most contractors can get approved—the difference is price, not eligibility.

Many contractors assume they won’t qualify due to credit—but the real risk isn’t approval, it’s what happens if your bond lapses or gets canceled. What Happens If Your Arizona Contractor Bond Cancels?

Related Pages:

Reviewed by: Jeremy Schaedler

Principal – Surety First Insurance Services

As principal at Surety First, Jeremy Schaedler has specialized in contractor license bonds and construction insurance since 2006. CA License: 0f06277

This information is for general informational purposes only and does not constitute legal advice. Licensing and insurance requirements may change. Contractors should verify current requirements directly with their state regulatory agency or consult qualified legal counsel.

Why Contractors Choose Surety First

- Specializing in contractor bonds and insurance since 2006 (20,000+ served)

- A-rated surety markets

- Fast approvals, often within minutes

- Direct state filing

- Serving contractors across CA, OR, WA, NV, AZ

Phone: 1-800-682-1552

Website: suretyfirst.com

Sources

- Arizona Registrar of Contractors

- https://roc.az.gov/

- Arizona Contractor License Requirements

https://roc.az.gov/license - Arizona Revised Statutes Title 32 Chapter 10

https://www.azleg.gov/arsDetail/?title=32 - Surety & Fidelity Association of America

https://www.surety.org - National Association of Surety Bond Producers

https://www.nasbp.org - Experian